IPOs: Profiles Are High. What About Returns?

Initial public offerings (IPOs) often attract initial public interest—especially when familiar brands become broadly available to investors for the first time. In recent months, investors have had the opportunity to buy shares of ride‑hailing networks Uber and Lyft, workplace productivity services Zoom and Slack, and other high-profile businesses ranging from Pinterest to Beyond Meat.

News outlets contribute to the frenzy, building anticipation, tracking the early hours of trading, and casting judgment on the IPO’s success. Investors, perhaps lured by tales of outsized returns, try to get in on the action early.

New Dimensional research reveals the fundamental challenges IPO investors face. They may not be able to trade during the early hours, when the biggest price movements frequently occur. Lockup periods also often restrict when shares held by early investors can be resold on secondary markets, which can limit meaningfully the available liquidity in the first six to twelve months after an IPO. And medium‑term IPO performance is often underwhelming.

Dimensional’s Research team studied the first-year performance of more than 6,000 US IPOs from 1991 to 2018 and found they generally underperformed industry benchmarks. The researchers also found that known drivers of expected returns largely explain that underperformance.

Short-term IPO Returns

IPOs are commonly associated with outsized stock returns on the first day shares become available, although these returns may not be attainable by all investors due to the allocation process. Researchers have shown that initial trading prices typically exceed the IPO offering price.1 However, accessing these first-day returns requires an allocation from the underwriting banks. Studies have documented an adverse selection problem associated with IPO share allocations and find that allocations to IPOs having poor first-day returns have generally been easier to obtain, while allocations to IPOs with good first‑day returns have usually been reserved for certain clients of the underwriting banks.2

Medium-term IPO Returns

Given that many investors may not be able to access these initial returns, Dimensional focused on the performance of IPOs in the secondary market. How do IPOs perform in their first year?

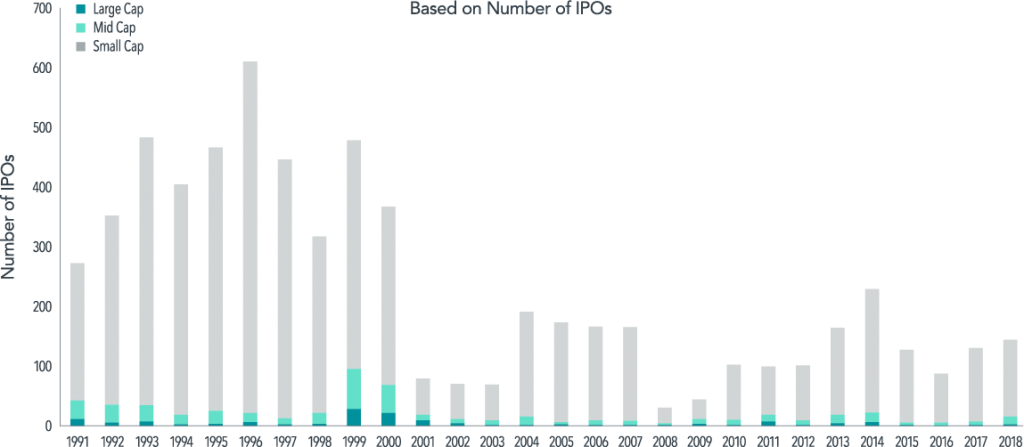

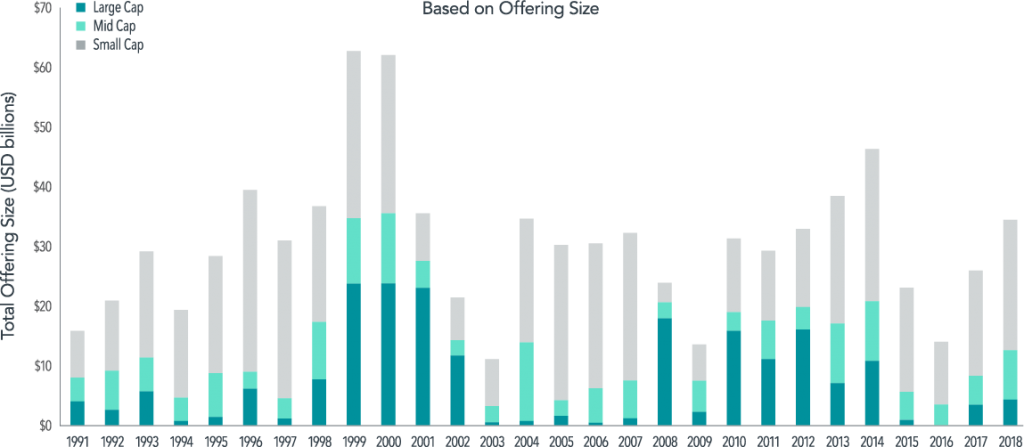

The sample for Dimensional’s study consists of 6,362 US IPOs that occurred from January 1991 to December 2018 and for which data is available.3 Exhibit 1 shows the annual frequency and market cap distribution of IPOs among firm size groups. The period from 1991 to 2000 is characterized by a relatively high IPO frequency rate of 420 per year and is followed by a less active 18-year period during which the rate falls to 120 IPOs on average per year. Although the number of IPOs has declined, the average IPO offering size is almost three times larger over the most recent period, as compared to the initial 10 years in the sample.

Most IPOs fall into the small cap size group, defined as firms that fall below the largest 1,000 US‑domiciled common stocks at the most recent month‑end. Large cap and mid cap IPOs represent 24% and 19%, respectively, of total capital raised through IPOs over the sample period.

Exhibit 1: Annual IPO Activity by Market Cap Size Group

Source: Dimensional using Bloomberg data. The sample includes US market IPOs, including US-domiciled companies and foreign-domiciled IPOs in the US, with an offering date between January 1, 1991, to December 31, 2018. Excluded from the sample are IPOs with an offer price below $5, unit IPOs (common stock and warrants), and IPOs involving real estate investment trusts, closed-end funds, American depository receipts, partnerships, and acquisition companies. IPO categories (small, mid, and large) are based on market cap rank relative to all US-domiciled common stocks as of the most recent month-end. Large, mid, and small cap are defined as firms that rank in the top 500, 501–1,000, and >1,000 by market value, respectively.

IPO Performance

Dimensional evaluated IPO returns by forming a hypothetical market cap-weighted portfolio consisting of IPOs issued over the preceding 12-month period, rebalanced monthly.4 This methodology excludes the initial first-day returns by design to alleviate the adverse selection problem inherent in the IPO allocation process. Exhibit 2 compares the returns of the IPOs to the returns of the Russell 2000 and 3000 indices over the full sample period as well as two subperiods covering 1992–2000 and 2001–2018. IPOs underperform the Russell 3000 Index in both the overall period and sub-sample periods. For example, IPOs generate an annualized compound return of 6.93%, 13.63%, and 3.74% over the full, initial nine-year and final 18-year sample periods, respectively, as compared to 9.13%, 15.70%, and 5.98% for the Russell 3000 index over the same time horizons. In comparison to the Russell 2000 Index, the hypothetical portfolio of IPOs underperform in the overall period (6.93% vs. 9.02%) and the 2001–2018 (3.74% vs. 7.29%) subperiod and outperform (13.63% vs. 12.56%) over the period from 1992 to 2000.

Known drivers of returns largely explain the underperformance of IPOs. IPOs have underperformed the market because, as a group, they have behaved like small growth, low profitability, high investment stocks, which have had lower expected returns than the market.5

Exhibit 2: IPO Returns Analysis

Past performance is not a guarantee of future results.

Source: Dimensional using Bloomberg data. The sample includes US market IPOs, including US-domiciled companies and foreign-domiciled IPOs in the US, with an offering date between January 1, 1991, to December 31, 2018. Excluded from the sample are IPOs with an offer price below $5, unit IPOs (common stock and warrants), and IPOs involving real estate investment trusts, closed-end funds, American depository receipts, partnerships, and acquisition companies. The hypothetical IPO portfolio is formed December 31, 1991, and is rebalanced monthly to include all firms with an IPO during the prior 12-month period. Weights are based on prior month-end market capitalization. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indices. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio

Summary

Investors considering IPOs should be aware of potential adverse selection and post-offering activities, such as the expiration of insider lockup periods. Investors should also understand that IPOs have generally underperformed broader market benchmarks in recent decades and that their fundamental characteristics suggest lower expected returns.

________________________________________________

1Ritter, Jay. 1987. “The Costs of Going Public.” Journal of Financial Economics 19: 269 -281.

2Reuter, Jonathan. 2006. “Are IPO Allocations for Sale? Evidence from Mutual Funds.” The Journal of Finance 61: 2289 -2324; Jenkinson, Tim, Howard Jones, and Felix Suntheim. 2018. “Quid Pro Quo? What Factors Influence IPO Allocations to Investors?” The Journal of Finance 73: 2303 -2341.

3Dimensional mirrors the traditional empirical research approach to analyze US IPOs by excluding the following: IPOs with an offer price below $5, unit IPOs (common stock and warrants), and IPOs involving real estate investment trusts, closed-end funds, American depository receipts, partnerships, and acquisition companies.

4Market cap figures are based on Bloomberg data that exclude shares subject to IPO lockup agreements.

5Black, Stanley and Kevin Green. 2019. “What to Know About an IPO.” Research Matters: 3.

________________________________________________

References

Black, Stanley and Kevin Green. 2019. “What to Know About an IPO.” Research Matters: 3.

Bradley, Daniel, Bradford Jordan, and Ivan Roten. 2001. “Venture Capital and IPO Lockup Expiration: An Empirical Analysis.” Journal of Financial Research 24: 465-493.

Brav, Alon and Paul Gompers. 2003. “The Role of Lockups in Initial Public Offerings.” The Review of Financial Studies 16: 1-29.

Ellis, Katrina, Roni Michaely, and Maureen O’Hara. 2000. “When the Underwriter Is the Market Maker: An Examination of Trading in the IPO Aftermarket.” The Journal of Finance 55: 1039-1074.

Fama, Eugene, and Kenneth French. 2015. “A Five-Factor Asset Pricing Model.” Journal of Financial Economics 116: 1-22.

Field, Laura and Gordon Hanka. 2001. “The Expiration of IPO Share Lockups.” The Journal of Finance 56: 471-500.

Hanley, Kathleen, A.Arun Kumar, and Paul Seguin. 1993. “Price stabilization in the market

for new issues.” Journal of Financial Economics 34: 177-197.

Jenkinson, Tim, Howard Jones, and Felix Suntheim. 2018. “Quid Pro Quo? What Factors Influence IPO Allocations to Investors?” The Journal of Finance 73: 2303-2341.

Reuter, Jonathan. 2006. “Are IPO Allocations for Sale? Evidence from Mutual Funds.” The Journal of Finance 61: 2289-2324.

Ritter, Jay. 1987. “The Costs of Going Public.” Journal of Financial Economics 19: 269-281.

________________________________________________