Addressing Three Common Investor Questions

In 2017, global markets moved up most of the year, but that surely wasn’t the case in 2018. In fact, we haven’t seen that type of volatility in U.S. markets for some time. In this article, we’ll address three of the most common questions we’ve heard from investors curious about how their investment strategy is performing.

Will rising interest rates hurt my bond investments?

When the Federal Reserve increases the Fed Funds rates, which they did four times last year, the interest rates we receive on our short-term bonds typically rise. Yet, rising interest rates are a double-edged sword. Higher interest rates mean that our bond investments will generate more income, but also that the existing bonds in our portfolio will likely fall in price. This is where investors typically have concerns about their bonds and rising interest rates.

Long-term bonds typically will decline more than short-term bonds when interest rates rise because long-term bonds are more sensitive to changes in interest rates.

We prefer using short-term bonds since we want our bonds to be the ballast of our investment ship, and long-term bonds may introduce additional risks (e.g., interest rate risk). Consider that the broad bond market index, which has a wide range of bond maturities including many with over 20 years, declined -1.8% from January 1 to November 30, 2018. However, shorter-term bonds, those with maturities between one and three years, gained 0.9% in that period. 1

While we can never know for certain, our use of short-term bonds seems set to do well versus the current interest rate increases the Fed is considering this year. These bonds are not as sensitive to changes in interest rates versus the entire bond market, and given that interest rates have increased over the last three years, we are now earning a reasonable level of interest income from our bonds. This should be sufficient to offset potential price declines from the estimated Federal Reserve interest rate increases. Finally, since our bonds are generally shorter term than the average bond investment, that means our bond investments mature faster. As those bonds mature, we get to reinvest in the new, higher-yielding bonds when they come out. So, gradual rising rates could continue to be a beneficial trend for our bond investments.

Why don’t we just invest in the U.S.?

The numbers don’t lie. U.S. stocks outperformed non-U.S. stocks in 2018. Taking an even longer view, U.S. stocks outperformed non-U.S. stocks over the last three- and five year periods. It is understandable that investors may want to stick with the better-performing market. So then, why should we invest outside the U.S.? Opportunity. As much as we believe America is home to the entrepreneur, innovation and new business ideas exist all around the world. Consider that 45% of the world’s stock market capitalization, 75% of the world’s gross domestic product, and 73% of all tradable companies are outside the U.S.2

There is value overseas, as non-U.S. companies are more reasonably priced than U.S. companies. StarCapital Research, a German asset manager, compiles and publishes global stock market valuations scores on 40 countries based on a collection of fundamental and technical measures. In its latest ranking, the U.S. stock market scored 34 on the list of 40. That means 33 countries have more attractive valuations than the U.S..

This doesn’t mean that we should abandon our U.S. stocks, and it doesn’t guarantee that the countries that are more reasonably priced will do better. But, it does show that combining stocks from the U.S. and non-U.S. opens the door to additional opportunities.

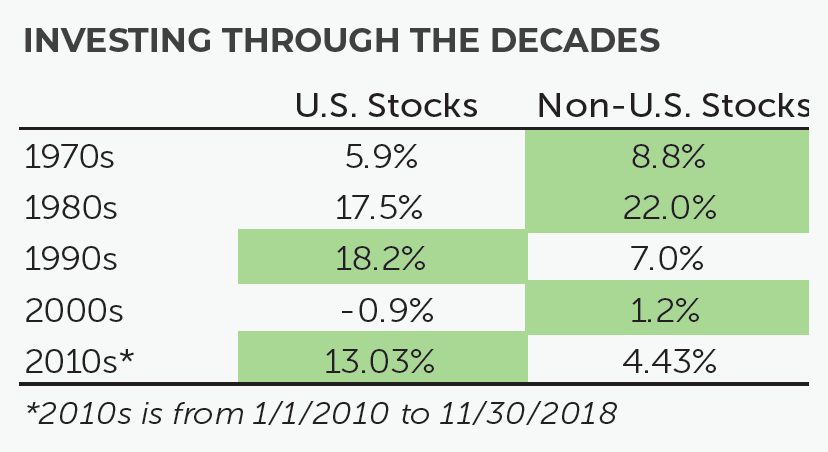

In fact, if we look decade by decade since the inception of the MSCI EAFE Index, an index of developed non-U.S. stocks, we can see that non-U.S. and U.S. stocks have flip-flopped in terms of outperformance (see chart below). U.S. stocks beat non-U.S. stocks in two decades, and non-U.S. stocks beat U.S. stocks in three decades.3 There is a diversification benefit to having both type of stocks in our portfolios.

When will we receive value from our value investing strategy?

While value stocks have had their moments from time to time, growth companies have been delivering impressive results over the past few years.

The Russell 1000 Value Index, which measures the performance of U.S. large cap value companies, returned an annualized 12.5% for the 10 years ending 11/30/2018. The Russell 1000 Growth Index, which measures the performance of U.S. large-cap growth companies, returned an annualized 16.5% for the 10 years ending 11/30/2018. That means that growth stocks outperformed value stocks by 4.0% every year.

This typically isn’t the case. History has shown us that value stocks tend to outperform growth stocks. But, while we expect value stocks to outperform growth stocks on a regular basis, the returns we receive from value stocks may not always be superior to growth stocks. In fact, we could go for an extended period of time before we see value stocks outperform growth.

To get an idea of how long we might have to wait to realize a value premium, researchers from the University of Chicago and Dartmouth College ran the numbers. Using a simulation technique where they use actual historical data to generate future probabilities, Eugene Fama and Ken French found that it isn’t uncommon for investors to have to wait more than 10 years to see value stocks outperform growth stocks (their simulation found that any given 10-year period could have a negative return premium 15.6% of the time). 4

This isn’t the only time we’ve seen value struggle versus growth. We saw growth stocks significantly outperform value stocks in the 1990s in the U.S. However, it didn’t take long for value stocks to come back and outperform growth stocks.

THE COMMON THREAD BETWEEN THE QUESTIONS

There are no givens when it comes to investing. The best we can do is try to manage the uncertainty — which is why we use a time-tested, evidence-based approach focused on pursuing opportunities that are based on sound theory and real results. We believe we align our investments with risks that are worth taking and try to avoid or minimize areas of the market where we don’t feel properly compensated for the risk we may take.